May 2026 - Snowballers

#UKSTOCKS #TBCG #MAB1 #CABP #ECEL #CTA

Introduction

This is the second “Snowballers” screen of 2026.

This is run 4 times a year, in February, May, August and November, thus providing a quarterly view.

You can view the full list of screens and schedule for 2026 here.

The Snowballers Screen

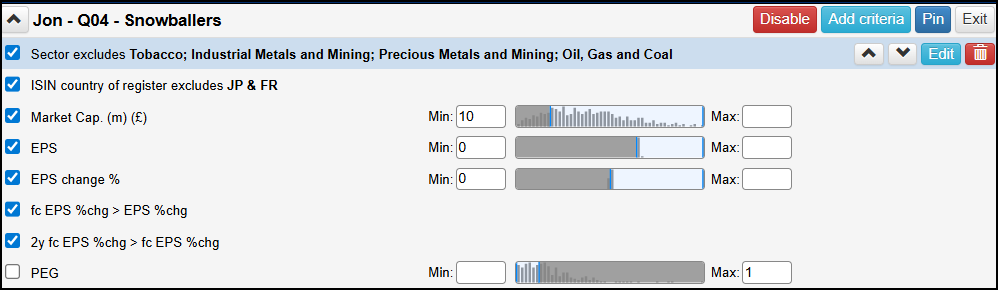

This screen is available in the Sharescope Filter Library, it’s titled “Briefed Up - Q04 - Snowballers”.

For those of you needing any orientation with filters, this Sharescope article is very useful, as it also includes details on how to access the library and these filters.

Do remember, for additional help and support, all Sharescope subscribers can book free training sessions here.

Frequency

Every quarter, on the third or fourth Sunday of February, May, August and November, 4 times a year. Apologies, this one is slightly late this month.

Objective

Identify stocks where this year’s earnings were greater than last year, and where they are forecast to grow exponentially next year and the year after.

Parameters

Stock Universe Settings

Market Cap: Default - £10m to No limit - To exclude small illiquid stocks

Sectors: Default - Exclude “Tobacco”, “Industrial Metals and Mining”, “Precious Metals and Mining”, and “Oil, Gas and Coal” - To exclude sectors I don’t typically invest in

ISIN Country of Register: Default - Exclude “JP” and “FR” - To exclude these specific foreign registered stocks

Note: My default stock list is always “LSE shares (excluding Investment Trusts (ITs))”.

Base Settings

EPS (this year) - Is greater than 0

EPS percentage change this year - Is greater than 0

Forecast EPS growth next year - Is greater than the EPS growth this year

Forecast EPS growth the year after next - Is greater than the Forecast EPS growth next year

Optional Settings

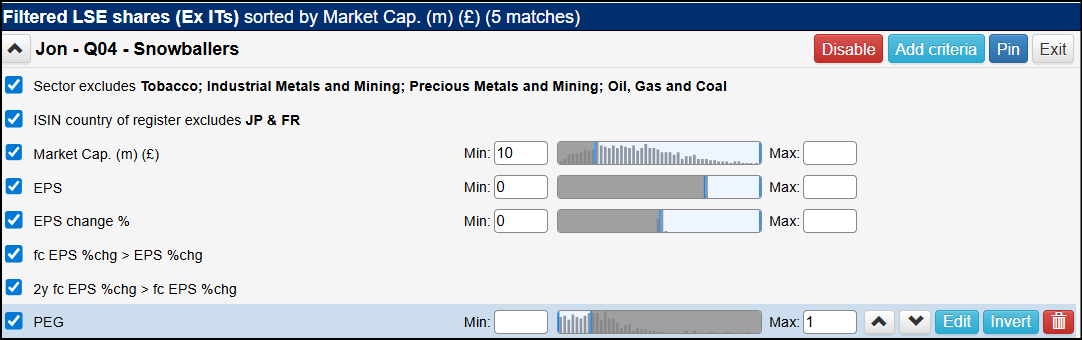

PEG - Is less than 1

Snowballers - This month…

The default settings returned 37 stocks, so I decided to tick the optional setting “PEG - Is less than 1” this month, which conveniently returned exactly 5 stocks.

Actual Settings

Results

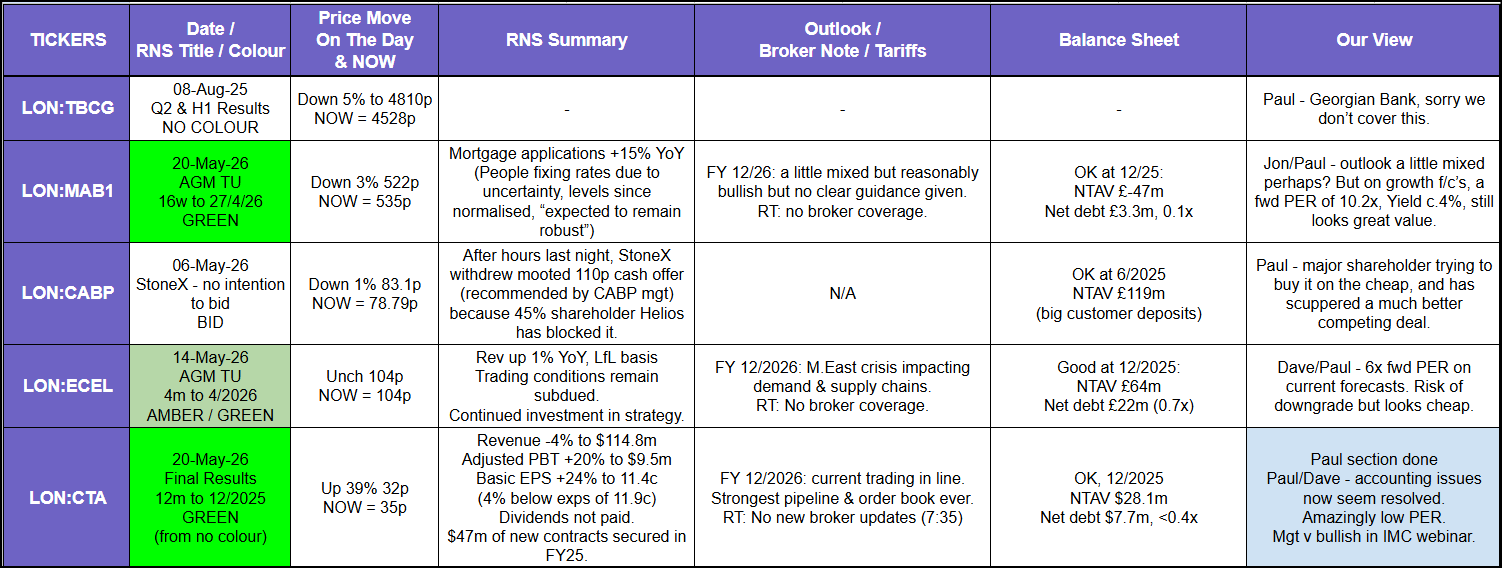

“Our View”

As usual, Paul has kindly allowed me to provide the current view from the Small/Mid Caps with Paul Scott Substack database for the 5 stocks I am covering this month, so here they are…

Members of the Small/Mid Caps with Paul Scott Substack can click here to access details and commentary for the vast majority of all of the stocks from the above results. The full history for most UK stocks is available via the the new Small/Mid Caps Value Report Search App, which covers over 18 months of updates in some cases.

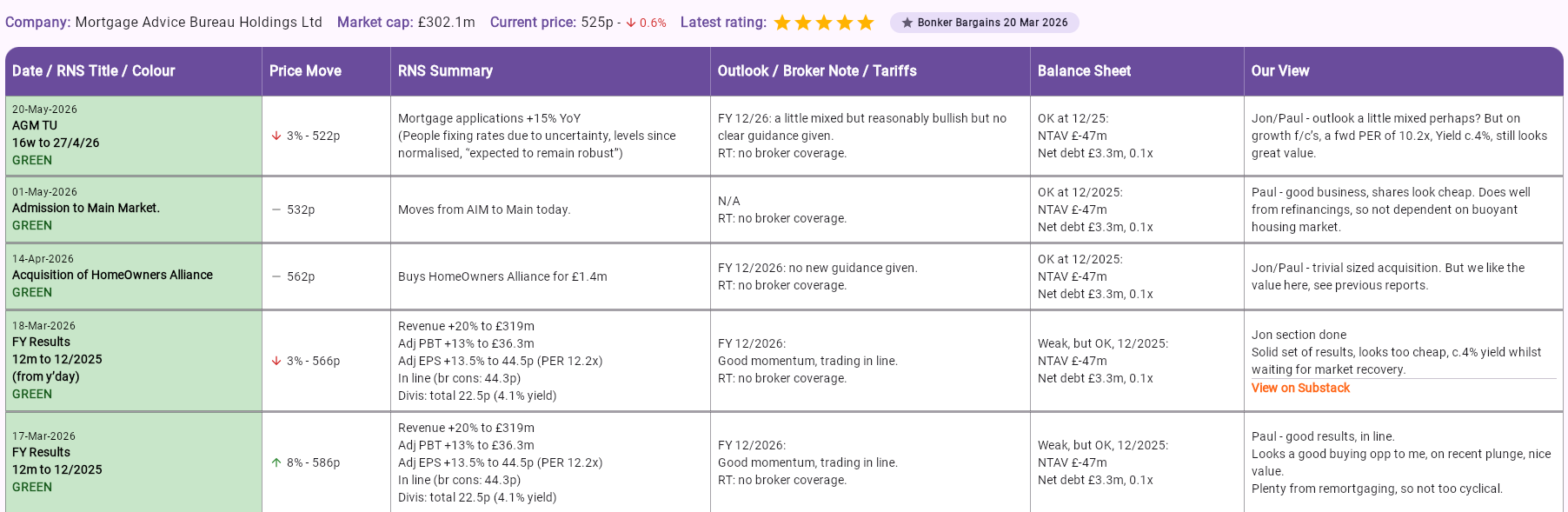

For example, here are the last five (of thirteen) Small/Mid Caps Value Report Search App entries for MAB1…

Note: As well as the five daily analysis table entries, the main article coverage for during the period (by yours truly), which can be accessed by clicking the link within the app.

Members of the Small/Mid Caps with Paul Scott Substack get:

Access to the complete history, and current view, of over 800 UK stocks via the Small/Mid Caps Value Report Search App

Main section articles on over 250 of those UK stocks

Morning RNS announcement analysis, out before the market open

Daily analysis of up to 30 stocks a day, even more on very busy news days

Exclusive interviews

Up to 5 podcasts a week. and a weekly update video

Access to an active and growing community of UK investors, where participation is encouraged

A team (which includes me) with almost 100 years of joint investing experience, focused on delivering the best coverage of the UK stock market

In Focus

TBC Bank Group (TBCG) - A banking group: Provides retail, corporate, and digital banking services across Georgia and Uzbekistan. This banking group always looks cheap, typically on a PER of 6 or so, on a 6% or so yield, and a PEG below 0.5. I’ve been watching this stock since the early 2020’s, just because it’s always shown up on one or two of my GARP/value screens, and I’ve always avoided it because of the location and associated risks. That situation has not changed today even though I’ve missed out on a bagger. And, in fact I could miss out on a bagger again if these forecasts hold up and sentiment towards the region improves, but at the end of the day, it’s just not a risk I wish to take.

Mortgage Advice Bureau (MAB1) - Leading UK mortgage-broker: Provides new mortgages, refinancing and general financial services through a franchise network. I really like this business and even though it’s not ideal macro at present for new mortgages, the refinancing business is doing a decent job at picking up the slack. On a single-digit PER, a 5% yield and mid-high teen forecast earnings growth, I view this as a real GAvRP share, the v being for very.

Cab Payments (CABP) - Global business-to-business cross-border payments and FX services, focused on emerging and frontier markets. This is a special (strange) situation. Since the beginning of February this year, there’s been a bun-fight going on here. It’s between Helios (a private equity firm and the largest shareholder, at 45%), StoneX (a Nasdaq-listed financial services company), and the Board. Basically the Board supports the higher offer from StoneX (110p (up from 95p originally), which they’ve recently withdrawn), but it keeps being blocked by Helios, who are trying to buy the company for themselves for around 85p. The story is something like that, and I am not sure I have seen such a situation before. Anyway, it’s just not something I wish to get involved in.

Eurocell (ECEL) - The UK’s leading manufacturer and distributor of PVC windows, doors, roofing, and other building products. On a PER of 6x or less and high-teen earnings growth, forecast for this year and next, this looks wrongly priced, especially if you take into account the 6%+ yield on >2x cover! It just seems the market is overly pessimistic here. There’s been reasonable sized management buys in the past 6 months (above the current share price), and I reckon ECEL would still look cheap even on a mild warning that saw forecasts cut by 25% or so.

CT Automotive (CTA) - Designer and manufacturer of interior components (cup-holders, arm-rests, interior lights, etc.) for global automotive brands. Just not sure what to say about this one. I spotted this as being crazy cheap around 12 months ago, bought some, but ran out of patience at the end of January, as the market failed to agree with me and then the CFO walked the plank. Since then (of course!) there’s been some positive news flow, a well received Investor Meet Company presentation, and seemingly, a change in sentiment towards the company. Paul actually covered CTA in detail on his Small/Mid Caps with Paul Scott Substack on 20 May here, and this was followed up with a reader’s article here on 25 May (both are well worth a read if you are interested in the company). My view is that, if the forecasts are to be believed, this is worth well over 100p, PER <4x, forecast earnings growth well over 2x that! I have yet to make my own mind up, as I thought this once before and the market failed to agree with me - Once bitten and all that!

Summary

The Small/Mid Caps with Paul Scott Substack

If you are not already a subscriber to the Small/Mid Caps with Paul Scott Substack and are interested in a 1 week FREE trial, click here to access all of the features mentioned above.

Sharescope

If you are not already a subscriber to the excellent Sharescope software we use every day over at the Small/Mid Caps with Paul Scott Substack, click here for the Small/Mid Caps with Paul Scott Substack deal and get:

A discount to the annual subscription fee

Access to this screen and all my other screens - Copy, amend and run them with your own parameters, as and when you want, across any markets you want to

FREE direct, in-house telephone, email, and chat support, 8am to 5:30pm

FREE one-to-one training with a Sharescope expert, as many sessions as you need

A 30-day money-back guarantee, for annual subscriptions and new subscribers only

Thank You

As always, if you have any suggestions for improvement, or any feedback at all, do please leave a comment.

Thanks for reading, and see you in the next one!

IMPORTANT NOTE: It is vital that you check all figures in this article for yourself, as they may be inaccurate or may have changed since publication.

MORE IMPORTANTLY: No investment advice intended, for information only, I may hold all, some, none, of the stocks mentioned in this article - Do Your Own Research!

Jon

Some great leads there. Thanks for your work